Retirement Readiness

Turn What You've Built Into Income You Cannot Outlive

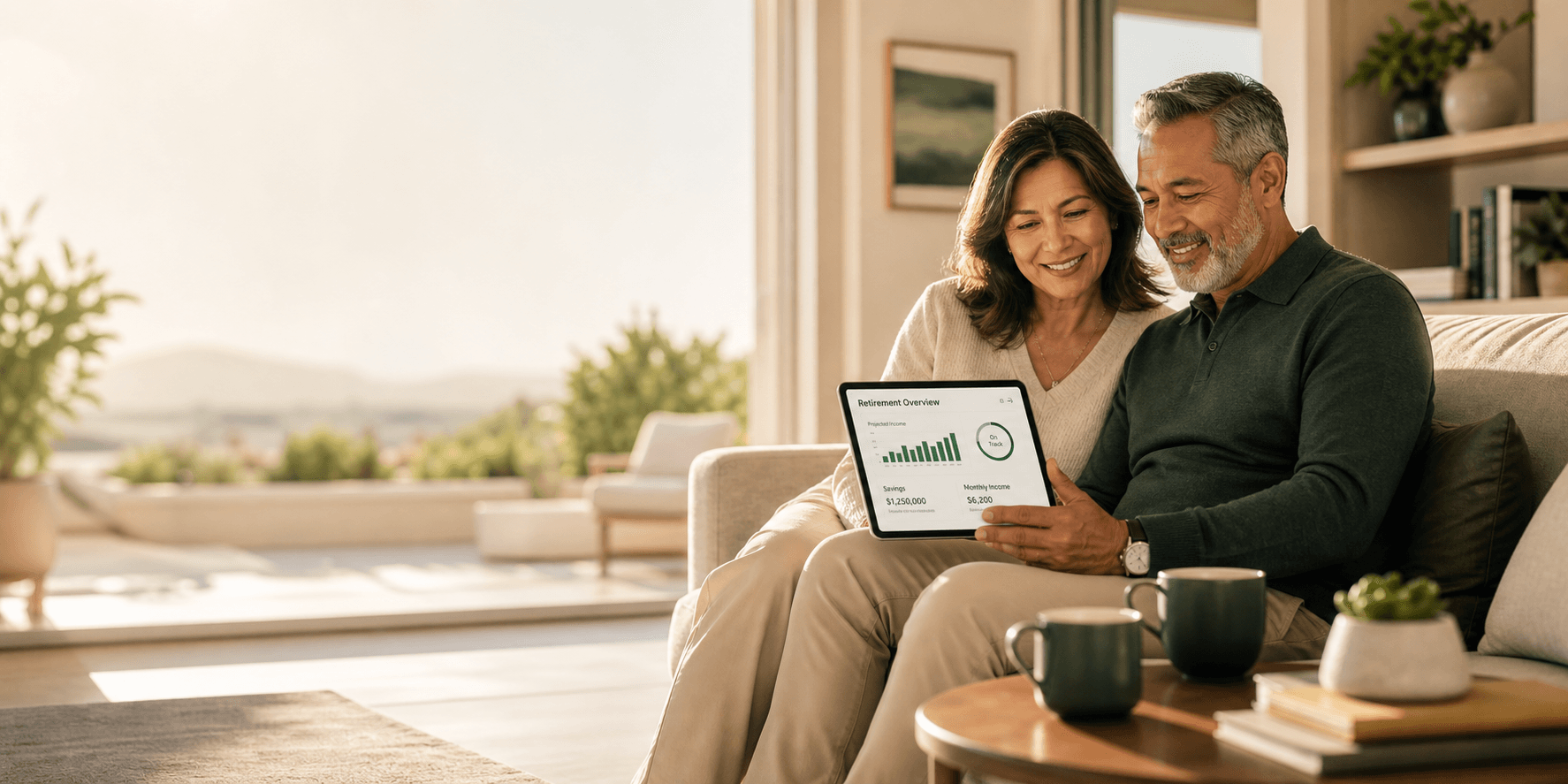

Convert what you have built into guaranteed, tax-efficient retirement income — with income you cannot outlive and a strategy that stops market volatility from derailing your plan.

How This Strategy Works

Income You Cannot Outlive

The greatest retirement risk is not a market crash — it is running out of money while still alive. A properly structured strategy creates guaranteed income regardless of how long retirement lasts, without depending on investment performance to pay the bills.

Tax-Efficient Distributions

Social Security, required minimum distributions, and investment income can push retirees into higher tax brackets than expected. Strategic positioning before and at retirement reduces the tax burden on every dollar of income — so more of what you saved actually stays in your hands.

Protected From Sequence-of-Returns Risk

A single down market at the wrong moment can permanently damage a portfolio that depends on liquidation. Floor protection strategies eliminate this risk at the exact moment it matters most — so your retirement income is not subject to market timing.

Retirement readiness is not about accumulation alone. It is about knowing that every year of retirement is funded, tax-efficient, and protected from the risks that cannot be predicted.

Complimentary. No pressure. A clear path to your LivingLEGACY™.

FAQ

Common questions about retirement readiness.

What is sequence-of-returns risk and how does KLG address it?

Sequence-of-returns risk is the danger that a portfolio decline early in retirement permanently damages withdrawals. KLG addresses this with floor protection strategies — fixed indexed annuities and IUL — that guarantee principal and income regardless of market performance.

How does a fixed indexed annuity provide income I cannot outlive?

A fixed indexed annuity structured with a lifetime income rider guarantees a minimum annual payout for life, regardless of how long the annuitant lives or what the account value does. The income payment continues even if the account value reaches zero.

What tax risks exist in retirement that KLG helps manage?

Required minimum distributions from qualified accounts, Social Security income being pushed into a higher tax bracket, and deferred tax liabilities being inherited by beneficiaries are the three primary risks. KLG addresses all three through strategic asset repositioning before and at retirement.